IN THIS ISSUE

💼 Your Bitcoin Wants a Job

💸 The First BTC Stock Exchange

🪙 Bitcoin’s Takeover of Visa and Mastercard

📈 Weekly Market Review

Jakob TL;DR

Your Bitcoin called with a reminder that Bitcoin can earn. It wants a job, let’s put it to work. I’ll speak at the Stacks Bitcoin Capital Markets webinar this Monday. Tune in to learn how Hermetica unlocks institutional-grade BTC yield.

This week was full of announcements that show a financial stack forming around Bitcoin as the base unit. Roxom launched the first stock exchange denominated in BTC. Bitcoin also achieved another financial milestone; it settled $6.9T over the last ninety days, matching Visa and Mastercard combined.

Your Bitcoin Wants a Job

Your Bitcoin called. It wants a job.

Jakob will be on a panel at the Stacks Bitcoin Capital Markets webinar this coming Monday, December 15th at 11am ET. Join him to learn how Hermetica unlocks institutional-grade on-chain BTC yield with real-time transparency.

You might even catch an early glimpse of what’s coming soon…

The First BTC Stock Exchange

Stocks are no longer reserved for fiat.

Roxom has launched the first stock exchange that is fully denominated and settled in Bitcoin. Public Bitcoin Treasury Companies are traded directly against BTC.

Investors can now measure performance and risk in BTC, not dollars.

This happens as corporate Bitcoin exposure increases rapidly. According to Glassnode, public companies now hold 1M+ BTC on their balance sheets, up 800K since January 2023. Yet almost all of that activity still runs through fiat rails, a mismatch for investors who think in Bitcoin. Roxom is one of the first trading venues built to resolve that: prices, P&L, and market structure are all expressed in BTC from the start.

The same realignment is happening on-chain. Just as Roxom consolidates treasury-focused equities into a BTC-denominated exchange, hBTC consolidates institutional-grade bitcoin yield into a single on-chain protocol. Both move key pieces of the financial stack, equity and yield, out of fiat and rebuild them around Bitcoin as the reference unit.

Whether on-exchange or on-chain, finance is starting to regroup around BTC.

Are you ready to operate in that system, with end-to-end Bitcoin?

Bitcoin’s Takeover of Visa and Mastercard

You’ve probably heard the line: “Bitcoin is a reserve asset.”

However, that framing undersells Bitcoin’s role in settlements.

Over the last 90 days, Bitcoin settled $6.9T in value, according to Glassnode, rivalling the combined payment volume of Visa and Mastercard over the same period. Visa processed $4.25T, and Mastercard $2.63T, for a total of $6.88T.

Most of Bitcoin’s volume comes from large, high-value transfers. Bitcoin functions as a global settlement layer where major economic value moves and finalizes.

This is how value moves today. Quietly, a new financial system is emerging. One where Bitcoin anchors the rails and earns yield, instead of acting as a passive reserve.

Market Review

Bitcoin is trading below $92,000, up from a low of $80,000 three weeks ago. Five of the past eight Decembers delivered negative returns for Bitcoin.

Equities have also recovered from recent lows. The S&P 500 is within 1% of its highs, while the NASDAQ is more than 2% below its peak. The tech and AI-driven rally that has led markets since April has slowed. Nvidia, previously the market leader in the AI trade, is now roughly 15% below its highs.

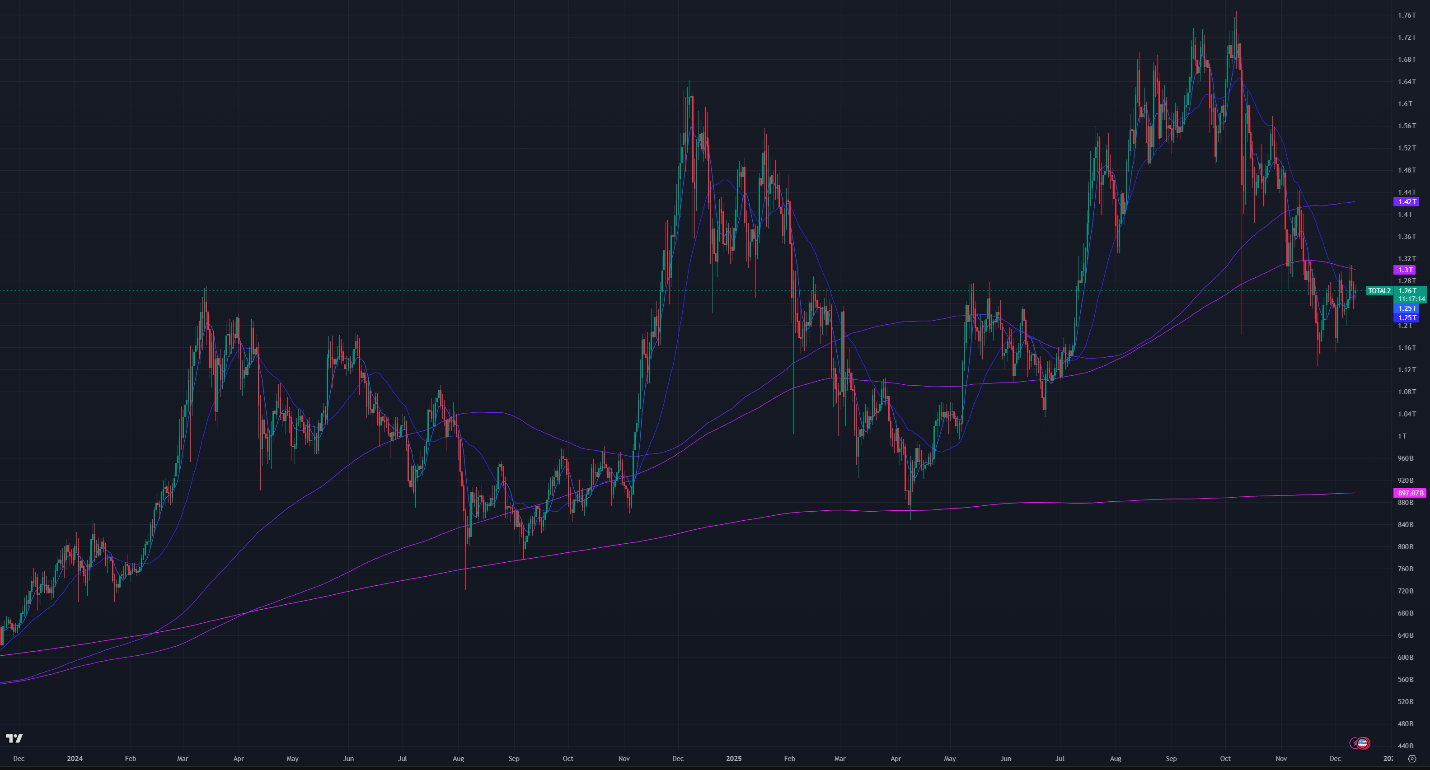

Aggregated altcoin market caps are at $1.26T. Bitcoin dominance is down 0.2% this week, extending a 1.3% drop from recent highs.

Data Summary:

DVOL: 43.32%

Equal-weighted futures basis spread: 4.59% APR

Futures curve is in an inverted contango from front week onward

Perp funding rates remain near zero

Figure 1: BTC Price, Daily Candles, & Moving Averages; 2 years; Source: Binance

Figure 2: Crypto Market Cap Excluding Bitcoin, Daily Candles, & Moving Averages; 2 years

Figure 3: Bitcoin Dominance, Daily Candles, & Moving Averages; 2 years

The moving averages (MA) in Figure 1 are:

Current Price: $92,100

7-Day MA: $91,400

30-Day MA: $90,900

180-Day MA: $109,000

360-Day MA: $102,200

200-Week MA: $56,200

Bitcoin price is just above the 30-day and 7-day moving averages (MAs), indicating that price is not in a strong downtrend. However, it remains below the longer-term 180-day and 360-day MAs, meaning a confirmed uptrend has yet to form. Price action has stabilized after the recent decline

From a technical perspective, $92,100 is acting as near-term support. Below this level, meaningful support is limited until lower prices. Key downside support levels are $86,000, $80,000, $76,000, and $60,000, with the 200-week moving average near $56,000 serving as critical long-term support, a level that has historically marked cycle bottoms.

BTC ETF Flows

Net inflows totaled $292M this week. Flows have cooled since Thanksgiving and are expected to remain subdued into Christmas and the New Year, reflecting typical year-end seasonality.

Figure 5: Bitcoin ETF Flows, Daily Bars; Source: The Block

Volatility

Bitcoin’s implied volatility (DVOL) is 43.32%, down from 47.27% last week. Since the October crash, volatility has remained between the low 40% and low 50% levels, with that range typically breaking when Bitcoin trades below $90,000.

Volatility trends lower over the long term, driven by market-maker options hedging across Bitcoin-linked products such as ETFs, Bitcoin treasury companies, and miners. Hedging compresses Bitcoin implied volatility and influences price behavior around key option expiration levels.

Figure 6: DVOL 2 Years; Bitcoin Index Price; Source: Deribit

Basis Spread

The basis spread, or the price of the futures contract over its spot price, is positive across all maturities. The average (equal weighted) basis spread increased from 3.83% APR to 4.59% APR week over week.

The futures curve is in inverted contango, with the front month (December 26) trading above later maturities. The spread between the lowest and highest yielding contracts contracted from 4.43% to 1.81%.

Figure 7: Futures Curve; Maturity Date, APR %

Macro

On December 10, the Federal Reserve concluded its eighth and final FOMC meeting of the year and cut the federal funds target range by 25 bps to 3.50%–3.75%.

In October, Powell emphasized that a cut was not guaranteed, citing the lack of economic data. Powell’s statement tempered near-term easing expectations and likely contributed to a sharp repricing in December SOFR futures. Expectations later re-stabilized. By the week heading into the December decision, markets had fully priced in the quarter-point cut.

Sincerely,

The Hermetica Team